The Real 3% investment option has delivered an annualized return of roughly 5.5% over the past decade, with no interannual volatility—an appealing stability virtually unmatched in the investment world. By contrast, the Cash Balance equity investment options have generated higher long-term returns, typically between 5% and 12%, but with annual fluctuations often exceeding 10% and sometimes 20% or even higher. Why would anyone willingly accept that kind of uncertainty? Because higher volatility tends to be correlated with materially higher long-term returns. Over a 30-year career, even a modest 3-percentage-point improvement in annualized return can multiply your ending balance fourfold. Starting with $100,000, that’s the difference between roughly $250,000 and $1 million—and that’s before considering the added benefit of making contributions during market downturns, when your new compensation deferrals into the Cash Balance are, in effect, credited as if you were purchasing more of a temporarily discounted asset.

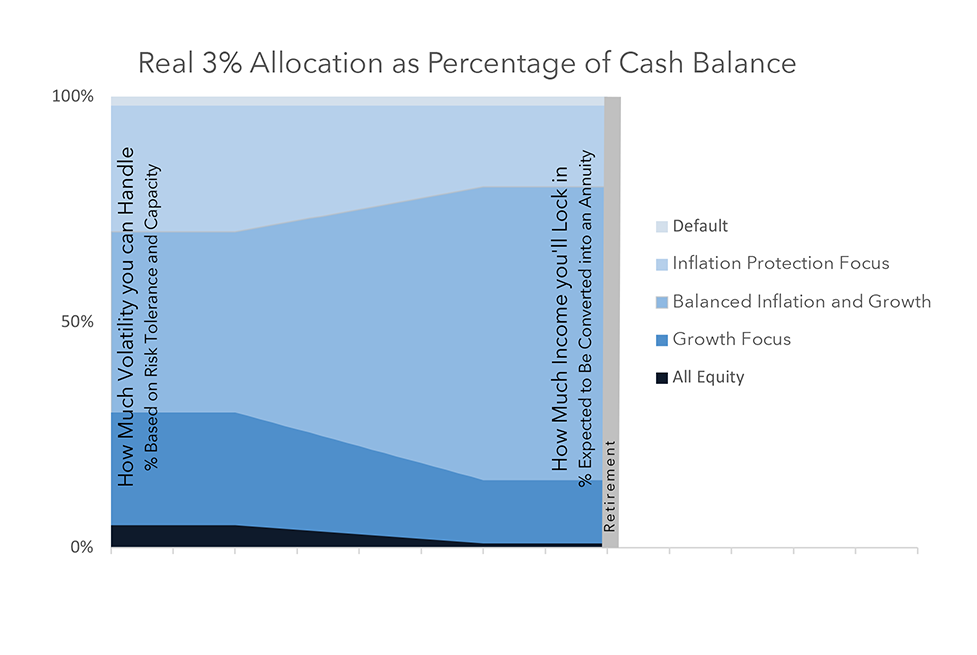

For WBG staff, the “right” allocation to Real 3% cannot be determined by performance history or return expectations alone. The key is recognizing that your Cash Balance often serves two distinct purposes—with two distinct time horizons. The portion you expect to convert into a lifetime annuity (if any) has a finite horizon: the date when you retire or begin drawing income. The remaining portion—typically rolled over to Individual Retirement Accounts (IRAs) to defer taxation if applicable, and to keep the funds invested or ultimately pass them to heirs—has a much longer horizon, extending through your lifetime and beyond. This distinction in purpose and timing ultimately shapes the appropriate balance between Real 3% and equity options.

Those who anticipate converting a meaningful share of their Cash Balance into an annuity will want to think of that fraction as a “shorter-term” portfolio: one that will soon need to be stable and ready for conversion regardless of market conditions. For that slice, often a somewhat gradual move toward Real 3% in the years leading up to retirement can help preserve value and reduce the risk that market declines coincide with the annuity calculation date. The rest of the balance—what is not intended for conversion—can remain invested aligned with risk tolerance, often for growth, reflecting the much longer horizon of your retirement years and your beneficiaries.

The “my HR Pension“ Benefit Calculator is an excellent tool for running “what if” estimates and exploring your “Payout Options” for annuity conversion, but it cannot determine your optimal Real 3% allocation. That decision requires a broader personal finance perspective—one that integrates your total resources, spending goals, and both your risk tolerance and capacity. In other words, while the Calculator can model the mechanics and illustrate potential outcomes, only you—potentially guided by a sound financial plan and an experienced financial planner—can determine how much, if any, of your Cash Balance should be anchored in Real 3%.

By understanding the split in time horizons and purpose within your Cash Balance, your Real 3% allocation becomes not a default setting but a deliberate choice—one that connects your investment posture today to the income security you will depend on tomorrow.